Overview

During the quarter, the global economy experienced a sharp retraction due to various measures imposed by governments. Over the past month, we have been encouraged by the return of economic activity with the gradual reopening of economies. While many sectors have been hard hit, the infrastructure sector has demonstrated its very high resiliency of cash flows. As we communicated previously, each of our businesses was deemed essential and has provided largely uninterrupted service throughout this challenging period.

Brookfield Infrastructure generated Funds from Operations (FFO) totaling $333 million in the second quarter, which was relatively consistent with the prior year. Our assets performed well on a local currency basis and only a very small portion of our overall revenue was affected by the global economic shutdown. Results reflect certain timing impacts that should be recovered over time. These include delays recognizing earnings associated with the buildout of a contracted backlog of projects in our U.K. connections business, and reduced traffic on our toll roads, for which we expect to be fully compensated under force majeure provisions in our concession agreements.

Across all geographies where we have GDP sensitive revenues, we have seen strong recoveries in volumes once restrictions were lifted. While we are pleased with the faster than expected recovery, many of these businesses are not fully back to pre-covid levels as certain safety protocols are inhibiting productivity at construction sites and commuter traffic levels are still impacted by employees continuing to work from home. We may not see a full recovery until later in the year or early 2021. However, barring any further shutdowns, the impact of the economic slowdown on Brookfield Infrastructure’s results in the next few quarters should be modest.

Over the past several months we have seen a significant rise in the stock market, as well as the recapitalization of numerous businesses impacted by the slowdown. Consequently, infrastructure asset values have held up and companies that we expected to sell assets to raise liquidity took on more debt as they were able to access the debt markets. Nonetheless, we have a strong pipeline of investment opportunities to deploy our capital and we remain patient in anticipation of large value opportunities that we believe will arise once stimulus measures abate. We have also relaunched various asset monetization opportunities, as the investment market for high quality essential businesses is robust. The stable performance of our mature assets throughout the height of the volatility underlines the value of essential infrastructure businesses. Consequently, we expect high levels of interest from prospective buyers.

Results of Operations

During the second quarter our business generated FFO of $0.72 on a per unit basis, down 5% from the prior year. The single largest impact on quarterly performance was the 27% depreciation of the Brazilian real which reduced FFO by $30 million. Adjusting for this alone, FFO per unit would have increased 3% compared to the prior year. Results for the quarter benefited from our capital recycling strategy. We deployed $1.2 billion of capital over the last 12 months at an average going-in FFO yield of 12%. These new investments were primarily funded with $1 billion of proceeds from asset sales and refinancing transactions at a much lower cost of capital. These positive factors were offset by lower market sensitive revenues, which were concentrated in our transport segment because of temporary lockdown measures. Overall, the impact of the economic shutdown reduced FFO by $27 million, with most of this being timing related, and therefore not expected to be a permanent loss.

Utilities

Our utilities segment generated FFO of $130 million, compared to $143 million in the prior year. Results reflected a higher rate base due to inflation-indexation and approximately $280 million of capital commissioned in the last 12 months. This segment also benefited from the contribution from our North American regulated gas transmission business acquired last October. These contributions were more than offset by a delay in the recognition of connections revenue at our U.K. regulated distribution business, the loss of earnings associated with the sale of an electricity distribution utility in Colombia and the impact of the weaker Brazilian real.

FFO for the quarter from our U.K. regulated distribution business was better than we expected. Construction quickly rebounded in May and June as homebuilders reopened their sites, with new connection activity averaging 65% of planned levels throughout June. While physical distancing protocols have limited our ability to add connections at full capacity, construction is now operating at approximately 85% of ‘normal’ levels and continues to improve. The business also recently secured its two largest capital projects of the year, representing approximately 28,000 new connections across four of our utility offerings. These initiatives reflect a rebound in building activity and the positive sentiment we are seeing from home developers. Moreover, this business stands to benefit further given recently announced stimulus to boost national housing demand – from early July 2020 until March 2021, the government has removed stamp duty tax on the first £500,000 of property value. Since these measures took effect, U.K. home sales are approximately 35% ahead of last year.

The privatization and de-listing process at our Colombian regulated gas distribution business is going as planned. In July, we completed a tender offer and successfully acquired a further 20% of the company for $90 million (BIP’s share – $25 million). We now own 75% of the business alongside our institutional partners. We are currently working through the final steps to de-list the company, which should be completed in the coming weeks.

The buildout of our electricity transmission operation in Brazil is progressing well. Despite the implementation of social distancing protocols, productivity is high and is generally consistent with prior years. We commissioned approximately 400 kilometers of transmission lines during the quarter and construction of the remaining 3,300 kilometers is on plan.

Transport

FFO from our Transport segment was $108 million compared to $135 million in the prior year. Results reflected higher volumes across our Australian and Brazilian rail networks, as well as the contribution from our recently acquired North American rail operation. These positive factors were more than offset by the loss of earnings associated with the sale of a European port business and the partial sale of our interest in our Chilean toll road operation. Results were also affected by a weaker Brazilian real and lower volumes following government-imposed lockdowns, which together reduced results by $29 million. Among these factors, (i) foreign exchange accounted for $14 million and (ii) $13 million relates to lower volumes at our toll roads, for which we expect to be compensated, based on force majeure protections and ongoing dialogue with local regulators. The true economic impact from the downturn is therefore limited to $2 million (or less than 1% of BIP’s total FFO) in our port operations.

Energy

Our energy segment generated FFO of $106 million compared to $96 million in the prior year. Performance was insulated from the current economic environment, as over 75% of cash flows are underpinned by take-or-pay contracts with an average maturity of 11 years. Results benefited from higher transport volumes at our North American natural gas pipeline, over 55,000 new customers at our North American residential infrastructure business and the contribution from the federally regulated portion of our western Canadian midstream business acquired in December. These contributions were partially offset by the loss of income associated with the sale of our Australian district energy operation completed last November.

Despite volatility in the global energy markets, our Canadian natural gas midstream operation recorded results that were ahead of prior year levels. This performance reflects the attractive contract profile, with over 85% of revenue earned under long-term, take-or-pay arrangements with primarily investment grade counterparties. Given the solid liquidity position of our counterparties, we do not foresee any significant concerns arising from a prolonged period of lower commodity prices. The Montney basin has impressive long-term economics due to high liquids yields, therefore most producers have a long-term supply cost less than current commodity prices.

Our North American residential energy infrastructure operation continues to operate with strong durability. Results reflect the fulfillment of good customer demand for cooling equipment, and our U.S. “sales to rental” strategy that has gained substantial momentum, achieving record HVAC rental conversion rates of over 55%. We are also making progress with our Canadian expansion outside of Ontario, having secured over 3,000 new long-term contracts in western Canada during the quarter. Following the securitization financing at our Canadian rental business in 2019, we have been exploring ways to further optimize our capital structure and efficiently fund growth. In that regard, we are working on a securitization financing at our U.S. business which we expect to have completed during the second half of the year.

The stability of our North American district energy operation has been showcased in recent months. This business serves a highly diversified customer base across multiple geographies and industries and generates almost all its EBITDA from volume agnostic capacity contracts. Throughout this period, we advanced several expansion projects and are seeing heightened interest from prospective customers looking to minimize the upfront capital spend associated with purchasing standalone heating and cooling equipment. Construction remains on target for the eastward and westward expansion of our Toronto system, which have the potential to collectively increase EBITDA by approximately $20 million when commissioned.

Data Infrastructure

FFO from our data infrastructure segment was $43 million, which was 43% higher than the prior year. Our French telecom business benefited from inflationary price increases and our build-to-suit tower program, which has added over 200 new sites. Results also reflected the contribution of earnings associated with recently acquired data transmission and distribution operations in New Zealand and the United Kingdom.

Our South American data center business finalized an agreement to build two new hyperscale facilities in Mexico that will add 36 megawatts of storage capacity over the next few years. These facilities will require $330 million of capital and are anchored by long-term, U.S. dollar denominated take-or-pay contracts with a leading global technology company. The initial phase is scheduled to come online in 2022 and is expected to contribute $50 million of EBITDA on a run-rate basis. Since investing in this business just over a year ago, we have increased contracted capacity by 24% and secured expansions into both Chile and Mexico, expanding the company’s existing footprint outside of Brazil.

At our New Zealand data distribution business, we have made progress with the margin improvement program that was core to our investment thesis. At the time of acquisition roughly one year ago, we identified a comprehensive multi-year, cost-out initiative to drive EBITDA margin expansion from low-20% to mid-30%. Our team is focused on reducing expenses, rationalizing non-core product offerings, and improving utilization of our utility-like broadband and wireless services. We expect these efforts, in combination with other activities underway, to result in annual FFO growth of approximately 10% over the next five years.

Our U.K. tower business continues to perform in line with our underwriting and has been successful in activating two new indoor systems in marquee buildings across the U.K. since closing at the end of 2019. This segment is expected to demonstrate good growth momentum as in-building connectivity remains a critical utility-like service for landlords and tenants with approximately 80% of mobile usage happening indoors. In light of this success, we are exploring the potential to export the in-building wireless model to other geographies where Brookfield has a large real estate presence to facilitate our market entry. Given the over 300 million square feet of owned office and retail real estate, we believe this could represent a significant growth opportunity.

Balance Sheet & Funding Plan

Our liquidity position is robust with approximately $4.3 billion of total liquidity, including approximately $3.2 billion at the corporate level. The business is further supported by a healthy investment grade balance sheet, and we have no material debt maturities for the next several years. During the quarter, Brookfield Infrastructure’s credit rating was reaffirmed at BBB+.

We have completed over $2.0 billion of financings so far this year. Our ready access to low cost debt capital is due to our conservative financing structures and many years of developing a track record as a high-quality borrower. We recently completed our first asset-level green bond issuance at the metered services operation of our North American residential energy infrastructure operation. The 10-year issuance of C$150 million priced at a coupon of approximately 3.8%.

Update on Strategic Initiatives

The economic cost of the downturn will be that many industrial companies and all governments will be significantly more indebted. Once the immediate measures to stabilize economies and businesses have been implemented, governments and businesses alike will need to evaluate alternatives to source capital to repay excessively high debt levels. We have spoken in the past about the secular trend of governments seeking investment from the private sector to acquire and build out infrastructure. With inflated deficits, along with the desire to stimulate economic activity, we expect the impetus for this to become even more pronounced. In addition, many corporations will be susceptible to tighter credit markets and they will need to reduce debt levels through asset sales. Suffice it to say, this is an attractive environment for Brookfield Infrastructure to source investment opportunities for the foreseeable future.

At the moment, the vast majority of our global investment team have returned to the office, which has reinvigorated our transaction and outreach activities. We are currently focused on executing several medium sized tuck-in acquisitions for various businesses in our energy, transport and data operations. As a result of the potential synergies, we believe that these acquisitions should be highly accretive if secured. Furthermore, we are evaluating numerous new investment opportunities in all of our regions.

During the quarter we made progress on various initiatives:

- North American Electricity Transmission –The sale of our North American electricity transmission operation closed in July, resulting in $60 million of proceeds to BIP and an IRR of 21%. We are advancing two other asset sale processes that we expect will generate over $700 million of additional liquidity. We believe that essential and de-risked infrastructure businesses that performed uninterrupted throughout this recent period will attract strong interest at premium prices.

- Indian Telecom Towers–The closing of our large-scale acquisition of 130,000 telecom towers in India from Reliance Jio is expected shortly. We have received positive feedback recently from Indian regulators that the remaining approvals are on track. Since we signed our deal, Reliance Jio has raised approximately $20 billion of equity capital from technology companies and private equity investors which has further solidified the credit quality of our anchor tenant. We will invest approximately $500 million of equity (BIP’s share) in the business.

- Capital Markets Investments – During the broad market sell-off in March, we acquired stakes in several high-quality infrastructure companies at attractive entry points. The ensuing rebound allowed us to monetize some of our positions and realize substantial profits in a short period of time. We have fully exited a number of these investments, realizing total profits of approximately $40 million (BIP’s share – approximately $25 million). We continue to accumulate positions in a handful of companies that we hope will lead to broader strategic initiatives in time.

- U.S. Midstream – Dislocation in North American energy markets may provide unique opportunities to invest at value. Our focus is on highly contracted businesses with solid counterparties, limited exposure to volume and pricing risk and long-life, critical infrastructure that complements our existing operations. We believe several opportunities exist to implement this strategy, both in the public and private markets.

Lastly, we are very pleased with the market’s response thus far to Brookfield Infrastructure Corporation (BIPC). Not only has there been significant demand for these shares but BIPC was also recently added to the Russell 2000 Index. We intend to support the growth of BIPC’s public float to improve the company’s trading liquidity, and recently completed our first initiative in this regard in coordination with Brookfield Asset Management, who agreed to sell a portion of its holdings in BIPC. This successful secondary offering in Canada increased the public float of BIPC by approximately 15%.

Resiliency in Uncertain Times – Spotlight on Regulated Terminal

We often characterize BIP as an investment for all seasons, highlighting the recession resistant characteristics of our business. Our cash flow profile is stable and predictable which is a function of the regulated and contracted nature of our assets.

A great example of this resilience through market cycles is our Regulated Terminal in Australia. As background, the terminal serves as a critical link in the global steel supply chain from one of the highest-quality and lowest-cost basins in the world (the Bowen Basin). This fully regulated terminal operates under an established regime and has long been a steady contributor within our utilities segment.

The business has the key characteristics that we look for in infrastructure assets:

- Strategically important asset that is an essential link to global export markets and supported by a high-quality and long-life resource

- Established regulatory framework provides a utility-like risk profile, and stable and predictable cash flows with a full pass-through of operating and maintenance costs

- No volume or commodity exposure as revenues areearned under long-term, take-or-pay arrangements

- Robust downside protection with a mechanism for socializing costs amongst counterparties in the event of a default and no force majeure provision in customer contracts

- Creditworthy counterparty profile comprised of some of the world’s largest mining companies

For these reasons, the economic slowdown had virtually no impact on the operational and financial performance of the business. Similarly, in the past, we have had experiences with extreme weather events, where this business continued to receive full revenue payments despite the terminal being unable to operate for periods of time.

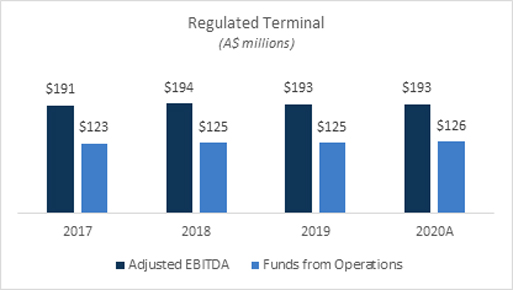

To better illustrate the strength of this business, in the following chart we have compiled annual EBITDA and FFO (annualized for 2020) since 2017. As can be seen, in the years between regulatory resets, the annual variability in both EBITDA and FFO is close to nil. Quarterly variability is also very limited as the business has no seasonality associated with its cash flows.

Brookfield Infrastructure acquired the Regulated Terminal at an attractive entry point in 2009, as part of the multi-faceted recapitalization of Babcock and Brown. Over 10 years of ownership, we have created value in several ways – (i) we executed significant capital projects that increased the regulatory rate base, (ii) we enhanced operating efficiency by improving working capital requirements and (iii) we reduced the cost of capital through opportunistic financing initiatives. This has, to date, resulted in returns of close to four times our invested capital.

Outlook

Our outlook for the balance of the year is more optimistic than when we last reported in May. While we remain cautious with respect to potential setbacks in the global recovery, we are encouraged by the pace of reopening and strong performance of our businesses. Results for our assets that have volume exposure have been, for the most part, quicker to rebound than we initially anticipated. At many of our businesses, results are ahead of plan for the year as communities emerge out of lockdown and economic activity ramps up further. While our payout ratio in the first half of 2020 is higher than our target range, we believe it will normalize as economic conditions improve and the Indian telecom tower transaction closes. We expect this acquisition to be accretive to our overall cash flows.

In the second half of 2020, we will focus on the execution of capital recycling initiatives. We are confident that the merits of investing in mature, de-risked, cash flow producing infrastructure assets will be more appealing to prospective buyers than ever – particularly with the expectation for low interest rates for the foreseeable future.

Our investment teams around the world are pursuing a number of large and strategic investment opportunities as well as follow-on acquisitions. An ongoing area of focus for us is on data infrastructure. We believe the sector offers significant opportunities given the large-scale investments required to replace the aging copper infrastructure with fiber and upgrade wireless networks to the new 5G standards. With increasing demands placed on their capital, telecom operators are looking for funding partners to reduce the strain on their balance sheets and deliver the next generation networks required to support an increasingly interconnected society. We remain patient in this regard but believe we have laid a substantial amount of groundwork and will aim to advance these opportunities in the coming months. Our liquidity position, combined with access to several sources of capital, will allow us to move quickly when a catalyst emerges for such transactions.

On behalf of the Board and management of Brookfield Infrastructure, we thank our unitholders and shareholders and wish you continued health.

Sincerely,

Sam Pollock

Chief Executive Officer

August 5, 2020

Forward-Looking Statement

Note: This letter to unitholders contains forward-looking information within the meaning of Canadian provincial securities laws and “forward-looking statements” within the meaning of Section 27A of the U.S. Securities Act of 1933, as amended, Section 21E of the U.S. Securities Exchange Act of 1934, as amended, “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995 and in any applicable Canadian securities regulations. The words, “will”, “continue”, “believe”, “growth”, “potential”, “prospect”, “expect”, “target”, “should”, “future”, “could”, “plan”, “anticipate”, “outlook”, “focus”, “plan to”, derivatives thereof and other expressions which are predictions of or indicate future events, trends or prospects and which do not relate to historical matters identify the above mentioned and other forward-looking statements. Forward-looking statements in this letter to unitholders include statements regarding the likelihood and timing of successfully completing the transactions and other growth initiatives referred to in this letter to unitholders, the integration of newly acquired businesses into our existing operations, the future performance of those acquired businesses and growth projects, financial and operating performance of Brookfield Infrastructure and some of its businesses, commissioning of our capital backlog, availability of investment opportunities, including tuck-in acquisitions, the state of political and economic climates in the jurisdictions in which we operate or intend to operate, the expansion of our businesses and operating segments into new jurisdictions,, the adoption of new and emerging technologies in the jurisdictions in which we operate, performance of global capital markets and our strategies to hedge against risk in such markets, ability to access capital, anticipated capital amounts required for the growth of our businesses, the continued growth of Brookfield Infrastructure and its businesses in a competitive infrastructure sector, the effect expansion and growth projects of our customers will have on our businesses, and future revenue and distribution growth prospects in general. Although Brookfield Infrastructure believes that these forward-looking statements and information are based upon reasonable assumptions and expectations, the reader should not place undue reliance on them, or any other forward-looking statements or information in this letter. The future performance and prospects of Brookfield Infrastructure are subject to a number of known and unknown risks and uncertainties. Factors that could cause actual results of the Partnership and Brookfield Infrastructure to differ materially from those contemplated or implied by the statements in this letter to unitholders include general economic, social and political conditions in the jurisdictions in which we operate or intend to operate and elsewhere which may impact the markets for our products or services, the ability to achieve growth within Brookfield Infrastructure’s businesses, some of which depends on access to capital and continuing favorable commodity prices, the impact of political, economic and other market conditions on our businesses, the fact that success of Brookfield Infrastructure is dependent on market demand for an infrastructure company, which is unknown, the availability and terms of equity and debt financing for Brookfield Infrastructure, the ability to effectively complete transactions in the competitive infrastructure space (including the ability to complete announced and potential transactions referred to in this letter to unitholders, some of which remain subject to the satisfaction of conditions precedent, and the inability to reach final agreement with counterparties to such transactions, given that there can be no assurance that any such transactions will be agreed to or completed) and to integrate acquisitions into existing operations, changes in technology which have the potential to disrupt the businesses and industries in which we invest, the market conditions of key commodities, the price, supply or demand for which can have a significant impact upon the financial and operating performance of our business, regulatory decisions affecting our regulated businesses, weather events affecting our business, the effectiveness of our hedging strategies, completion of growth and expansion projects by customers of our businesses, traffic volumes on our toll road businesses and other risks and factors described in the documents filed by Brookfield Infrastructure with the securities regulators in Canada and the United States including under “Risk Factors” in Brookfield Infrastructure’s most recent Annual Report on Form 20-F and other risks and factors that are described therein. Except as required by law, Brookfield Infrastructure undertakes no obligation to publicly update or revise any forward-looking statements or information, whether as a result of new information, future events or otherwise.